The U.S. economy is demonstrating resilience, with modest growth projected to continue through 2024, avoiding a hard landing. Inflation has decreased toward the Fed’s target (CPI at 2.5% and PCE at 2.6%), while the labor market is cooling but remains stable. Following a 50 bps interest rate cut by the Fed in September, the macroeconomic environment has shifted to a monetary easing cycle, driving equities to new all-time highs and improving bond returns.

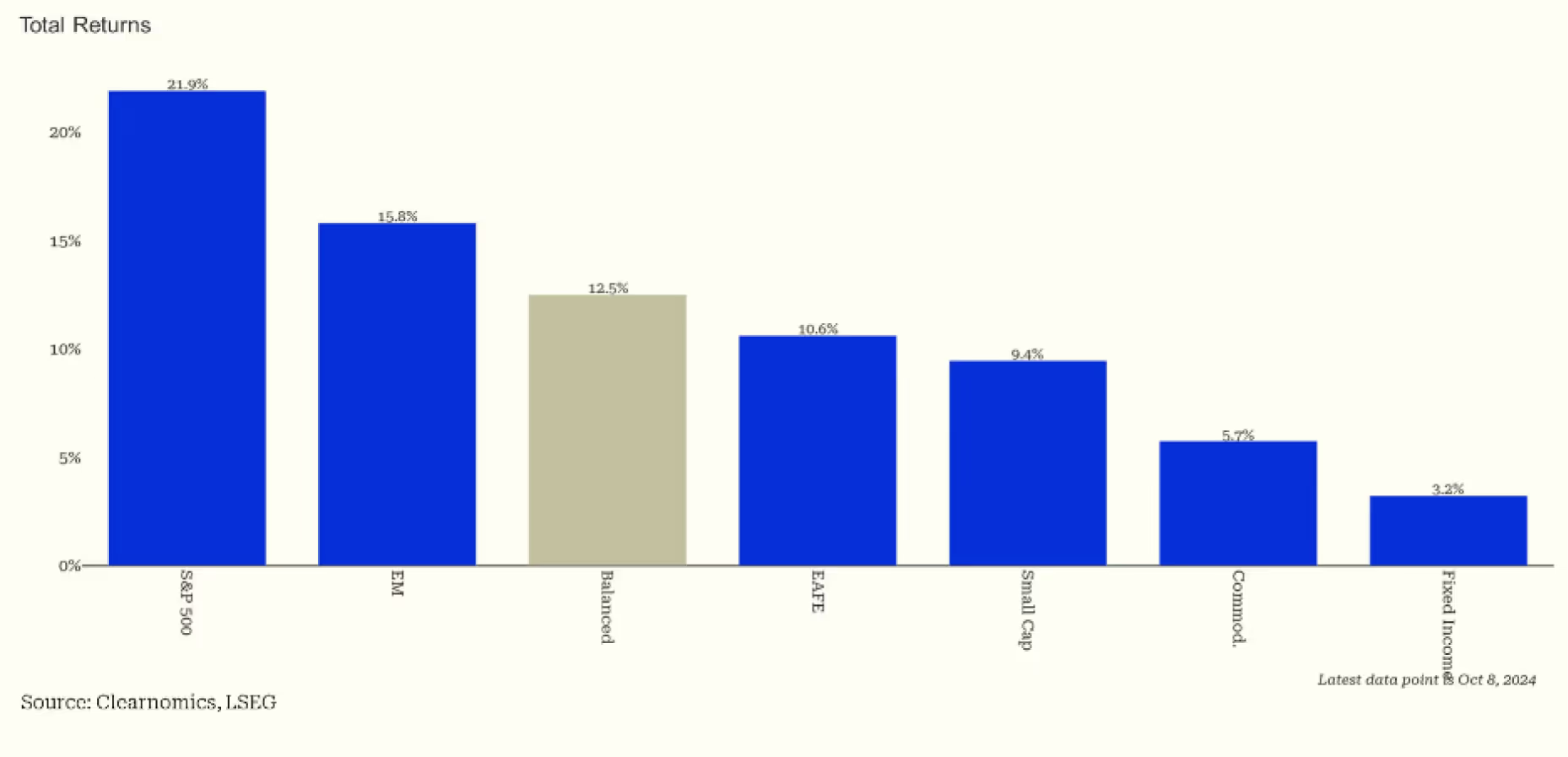

Figure 1: Asset Class Performance Year-to-Date

- The U.S. equity rally has broadened. Following a volatile August, the S&P was up 4% in Q3, the Dow Jones rose nearly 7%, and the Nasdaq fell 2%. Under the surface, returns differ due to a rotation out of the mega-tech stocks, which had driven most of this bull market. Instead, corners that had lagged – such as small company stocks and value stocks – are now performing well.

- The Fed rate cut in September resulted in lower interest rates across maturities and a “disinversion” of the yield curve, though markets may have overcorrected. Since the September nonfarm payroll (254,000 jobs added) and unemployment rate (4.1%) beat expectations, treasury yields have risen since the end of Q3 (2-year 3.99% and 10-year 4.06%, as of October 9th.)

- Q2 GDP grew by a healthy 3%. Wage growth has outpaced inflation for 17 consecutive months (4% year-over-year in September). However, the personal savings rate of 4.8% in August remains below the historical average of 8.5%.

- The technology sector continues to drive investment at unprecedented levels. Capital spending by the top five AI hyperscalers has surpassed $200 billion, supported by an influx of operating cash flow. The Chips Act of 2022 has further spurred semiconductor investments, with massive capital spending expected to continue.

- The price of gold has increased over 14% in Q3 and over 21% year-to-date. Gold prices have started to pull back as the USD’s strength has grown in Q4.

- Globally, developed markets returned 20.3% in Q3 as Japan equities recovered from early August sell-off. Emerging markets returned 23% – although after climbing 40% since September 10, China stocks plummeted following disappointing consumer spending figures.

Multiple risk factors remain in the months ahead:

- Future Fed policies remain uncertain. Stronger-than-expected economic data could lead to smaller rate cuts than anticipated.

- The upcoming presidential election could have significant impacts on tax policy, regulation, and trade.

- Geopolitical conflicts are worsening – with possible impacts on global stability, supply chains, and oil prices. As a result, we will likely see continued market volatility, with valuations and earnings expectations remaining elevated.

Ultimately, how investors choose to react to these factors will determine their financial success. Rather than trying to time the market to avoid risk, it is more prudent to build a well-constructed portfolio that can weather different market environments. Below, we provide further perspectives on these risk factors and how they might impact investors in the coming months.

1. The Fed is expected to cut rates further.

Moderate inflation and a cooling labor market set the stage for the Fed’s first rate cut in September, with more cuts expected through the rest of the year and into 2025. The market has been anticipating cuts of various sizes all year, rallying in the days following the announcement.

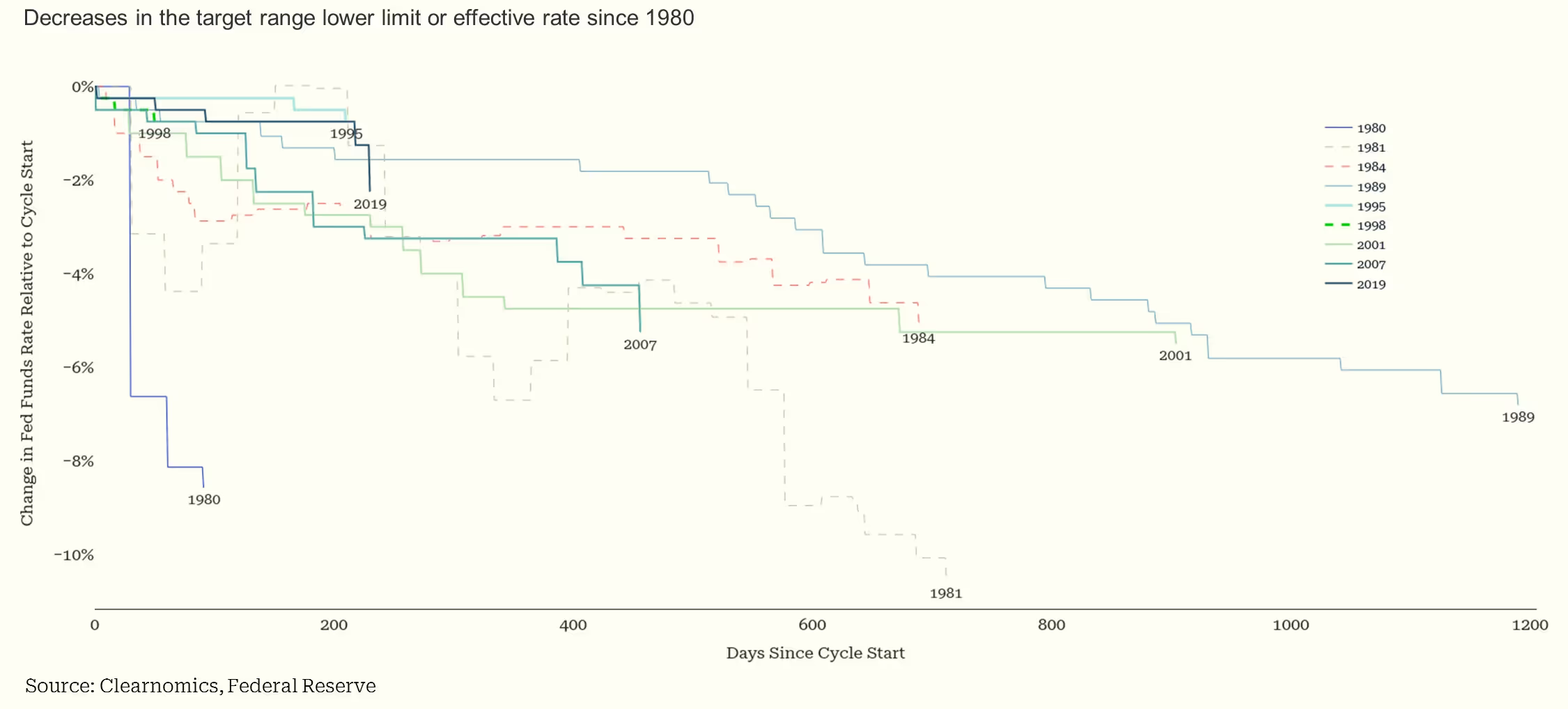

Figure 2: Fed Rate Cut Cycles

It is more important to analyze why the Fed cut rates, rather than when or by how much. Typically, the Fed cuts rates during economic and financial crises, such as in 2008 or 2020, constituting periods of time when the economy and market are expected to struggle.

In contrast, the economy is currently trying to achieve balance, or a so-called “soft landing,” just as the Fed did in the mid-1990s. The Fed’s rapid rate hikes in 1994 were followed by cuts in 1995, once inflation fears faded – which paved the way for economic expansion and a bull market. While this is only one example, it is important to draw the correct historical comparisons when it comes to Fed policy.

2. U.S. election: Vote not with thy portfolio.

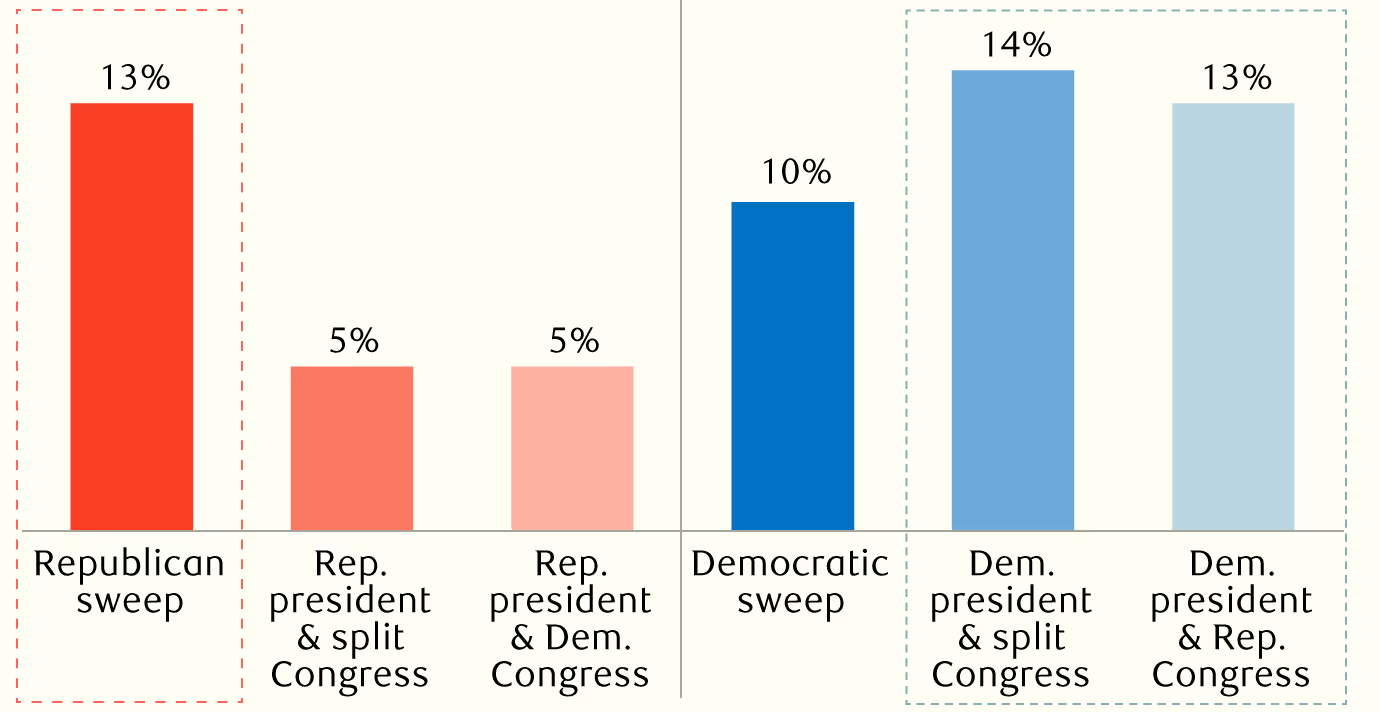

With the U.S. election in early November, future policies will hinge on which parties win the presidential seat and the majorities in Congress. Historically, the U.S. market has performed well during periods of divided government and with a Republican sweep.

Figure 3: Average annual S&P 500 returns when different political parties were in control of the federal government since 1932

Source – RBC Capital Markets U.S. Equity Strategy, Haver Analytics; based on price returns and does not include dividends

Please refer to our election analysis piece for more details. Our key message to clients on election when it comes to investments is:

- As the race intensifies, remember that while elections are important for the country, we should not vote with our portfolios and savings.

- The stock market has performed well under both political parties. The underlying drivers of market performance – economic cycles, earnings, valuations, etc. – are far more important than who occupies the White House or controls the legislature.

- That said, policies can certainly affect taxes, trade, industrial policy, regulatory frameworks, and more. However, what politicians promise is often different than what is ultimately enacted. Thus, investors should focus on long-term economic and market trends, rather than daily poll results. Investors concerned about the impact of specific policies on their financial strategies should work with a trusted advisor.

3. Geopolitical conflicts are worrisome, but do not directly impact markets.

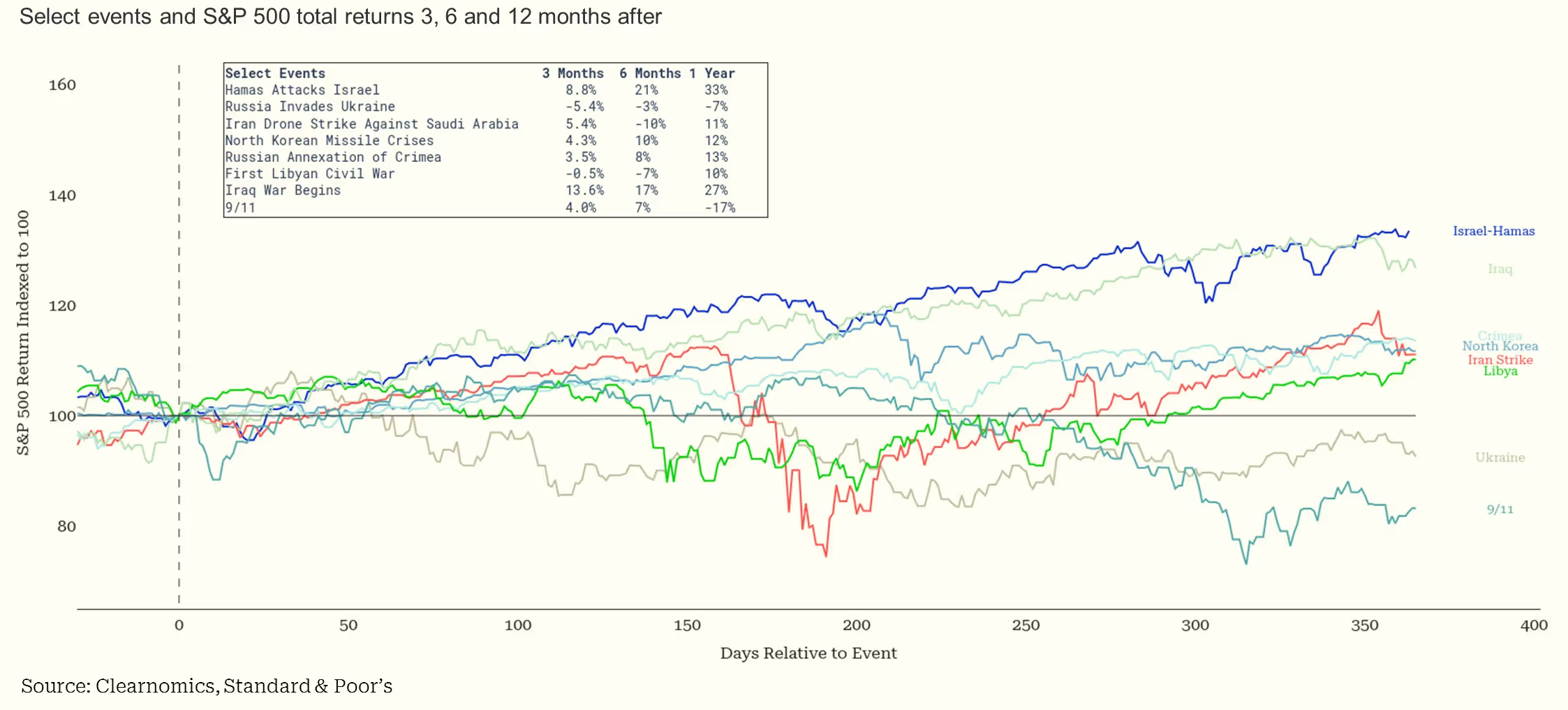

Figure 4: Stock Returns and Geopolitical events

Tensions have risen in the Middle East, as the conflict between Israel and Hezbollah continues to intensify. This adds to global geopolitical tensions including the ongoing war between Russia and Ukraine. While these events have major real-world consequences, their effects on the economy and stock market are less definite; and any impact on investors’ portfolios is typically fleeting. As Figure 4 shows, periods with prolonged market downturns often coincide with major market events such as the Dot-com Crash or the 2022 rate hikes.

Despite geopolitical uncertainties, the stock market has experienced only two 5% or worse pullbacks this year – emphasizing the importance of staying invested and focusing on broader market trends, rather than reacting to headlines.

In terms of the broader economy: regional conflicts can greatly impact oil prices. While the escalation in the Middle East has caused a slight rise in oil prices, the increase is modest, compared to previous crises. The U.S.’s position as the world’s largest oil and gas producer may provide some insulation from global events.

From an investment perspective: navigating oil price fluctuations can be challenging, particularly if they are the result of uncertain geopolitical developments. The performance of the energy sector during periods of market stress illustrates this point. In 2022, when the broader S&P 500 index was down 18% and most sectors posted negative returns, the energy sector delivered a remarkable 66% gain. This followed a 55% return in 2021 for the sector, when the economy rebounded after the pandemic.

While past performance does not guarantee future results, maintaining a diversified portfolio that includes many sectors, including energy, can help investors offset the volatility resulting from rising oil prices. In the long run, holding a portfolio that can weather market swings allows investors to stay focused on their long-term financial goals.

We invite you to connect with your Farther advisor for any questions related to this month’s commentary.