Q1 2025: Tariffs, Turbulence, and Market Trends

April 3, 2025

“Because I could not stop for Tariffs –

They kindly stopped for me –

The Reciprocals resumed but just Trade Wars –

And inflation encore.”

— Inspired by Emily Dickinson

On April 2, 2025, President Donald Trump announced and implemented a sweeping set of reciprocal tariffs, surpassing expectations of a 10% baseline tariff. These measures extend far beyond those enacted during his first term, potentially impacting an estimated $3.3 trillion worth of imported goods – significantly higher than the $380 billion affected previously.

Financial markets responded with immediate volatility. As of April 3rd, the S&P 500 declined by 4.4%, the 10-year Treasury yield lowered to 4.0%, and the U.S. dollar weakened by 2.3%.

Key Details of the Tariffs

- A 10% baseline tariff was imposed on all U.S. trading partners.

- Additional “reciprocal” tariffs were introduced for approximately 60 countries, calculated based on the U.S. trade deficit relative to each country’s exports to the U.S.

- Notable tariff rates include: China 34%, Japan 24%, South Korea 25%, and the European Union 20%.

- These tariffs are compounded by previous measures, including a 25% tariff on imported automobiles and specific auto parts and an additional 20% on Chinese imports.

- Goods from Mexico and Canada that comply with the USMCA largely remain exempt, except for auto exports and select steel and aluminum products.

Implications for the U.S. Economy and Markets

According to Dr. David Kelly, Chief Global Strategist at JPMorgan, these tariff levels mark a return to historical highs reminiscent of the 1920s and 1930s (Figure 1). As a result, economists are adjusting inflation forecasts upward and raising recession probabilities while tempering expectations for corporate earnings and GDP growth.

For U.S. corporations, the ramifications are profound. Unlike the tariffs imposed during Trump's first term, which primarily targeted China and intermediary goods, the new policies are expected to drive companies toward domestic production – where labor costs are substantially higher – rather than leveraging front-shoring or near-shoring strategies. Automotive, Technology, Consumer Goods, and Pharmaceuticals are particularly vulnerable to cost pressures and supply chain disruptions.

Global trade partners will likely respond with countermeasures or negotiations. The European Union, for instance, faces a paradox: while retaliation may be politically expedient, refraining could allow greater intra-European trade opportunities. The U.S. dollar faces potential downside as foreign central banks may reduce U.S. Treasury holdings. However, a weaker dollar could enhance U.S. export competitiveness.

Figure 1: Average Tariffs on Imports

Source: JPMorgan Guide to the Markets

Q1 Market Recap

Financial markets reflected a mixed picture across asset classes during a volatile quarter:

- Equities: The S&P 500 declined -4.6%, the Nasdaq -10.4%, and the Dow Jones -1.3%.

- Fixed Income: The Bloomberg U.S. Aggregate Bond Index gained 2.8%, with the 10-year Treasury yield settling at 4.2%, down from its 4.8% peak in January.

- Commodities & Digital Assets: Gold surged to a record $3,122 per ounce, while Bitcoin declined to $82,421.

- Global Markets: Developed international stocks (MSCI EAFE) gained 6.1%, and emerging markets (MSCI EM) increased 2.4%.

Figure 2: Asset Class Total Returns YTD

U.S. Stock Market Stumbled in Q1

While this marks the first down quarter for U.S. equities since Q3 2023, it is well within historical norms. The S&P 500 has experienced negative returns in roughly one-third of calendar years (Figure 3), yet long-term trends favor growth, as periods of expansion have consistently outpaced downturns in both frequency and magnitude.

Markets have been propelled by large technology companies with high growth expectations, leading to elevated valuations. The path forward will likely hinge on corporate earnings and economic performance. Thus far, earnings-per-share growth for the S&P 500 has remained strong, with consensus estimates projecting up to 12% growth over the next year, though new tariffs could trim that by 1%.

Figure 3: S&P 500 Calendar Year Returns

Bonds Provide Stability Amid Market Uncertainty

In uncertain markets, bonds serve as a crucial counterbalance to stock volatility. When equity markets falter due to growth concerns, bond prices tend to rise as interest rates decline, making existing bonds with higher yields more valuable.

Many types of bonds have performed well this year, including Treasury Inflation-Protected Securities (TIPS), mortgage-backed securities, Treasurys, and corporate bonds. This marks a reversal from the past few years, when high inflation and rising rates created one of the most challenging bond environments since the mid-1990s. This shift underscores a core principle of successful investing – maintaining a well-diversified portfolio aligned with long-term financial goals.

International Markets Rebounded

Bonds weren’t the only asset class to see gains in the first quarter. International equities also posted positive returns, with both developed and emerging markets seeing growth. This recovery follows years of relative underperformance due to U.S. market dominance and global economic and geopolitical challenges. The weakening U.S. dollar further bolstered international stock returns, enhancing the value of foreign assets in local currencies.

These trends highlight the importance of diversification across asset classes, regions, and sectors. While a balanced portfolio may not always be the best-performing strategy in any given year, it helps create a smoother investment journey over time.

The Fed Holds Steady Amid Inflation Concerns

Inflation moderated in the first quarter but remained above the Federal Reserve’s 2% target. Headline inflation (Consumer Price Index) rose 2.8% year-over-year in March, while the Core measure (which excludes food and energy) climbed 3.1%. Meanwhile, consumer sentiment has softened, with the University of Michigan Consumer Sentiment Index falling to its lowest level since 2022.

Despite these pressures, the Fed held interest rates steady in March within a range of 4.25% to 4.5%. While recession probabilities have risen, they remain near historical averages, with Wall Street typically pricing in a 20% chance of recession – roughly once every five years.

Balancing these concerns, the economy continues to show resilience, supported by a strong labor market, steady consumer spending, healthy corporate earnings, and upcoming pro-growth policies. It’s worth noting that recessions triggered by external shocks, such as tariffs, often lead to temporary slowdowns, with recoveries following once the impact dissipates.

Figure 4: Consumer Sentiment Declined to a Historical Low

Tariffs and Inflation: A Measured Fed Response

Households remain concerned about inflation, with long-term expectations reaching 4.1% – the highest level in three decades – amid anticipation of higher prices due to tariffs. Yet, consumer spending has remained relatively stable, buoyed by a strong job market, wage growth, and financial stability across many households.

In its March projections, the Fed slightly downgraded its economic outlook, forecasting GDP growth of just 1.7% for the year – the lowest since 2022. While the job market remains strong, persistent inflation remains a challenge.

Still, the Fed has chosen not to react aggressively to trade-related inflationary pressures (Figure 5), instead viewing them as “transitory.” Historical examples, such as 2018 tariffs on washing machines, suggest that while initial price increases occur, they often stabilize over time. The Fed’s cautious stance reflects its dual mandate of maintaining maximum employment and price stability, rather than overreacting to short-term fluctuations. That period also underscores the fact that tariffs were used by the first Trump administration as a negotiating tactic to achieve longer-term trade deals.

Figure 5: Historical Interest Rate Cycles

Rate Expectations and Market Implications

Although the Fed held rates steady in March, it still anticipates two rate cuts in 2025 (Figure 6), and market-based forecasts suggest the possibility of two or three cuts. However, rate expectations can shift quickly – at the start of 2024, markets priced in seven to eight cuts before expectations fell to zero. The actual number of cuts may change, but the overall trajectory of Fed policy remains supportive.

Additionally, while the Fed did not lower rates, it did signal a slowdown in its balance sheet reduction, effectively providing more liquidity to the economy. This adjustment, often referred to as quantitative tightening, could help ease financial conditions even without an outright rate cut.

For investors, the key takeaway is to focus on the long-term path of interest rates rather than short-term policy shifts. Historically, declining rates have supported economic growth and market performance by making borrowing more accessible.

Figure 6: Federal Reserve Dot Plot

The Role of Cash in a Long-Term Strategy

With interest rates still elevated, some investors may be tempted to hold excess cash for safety. While understandable, maintaining an overly conservative allocation can be counterproductive. Markets often rebound when least expected, and sitting on the sidelines can derail financial plans.

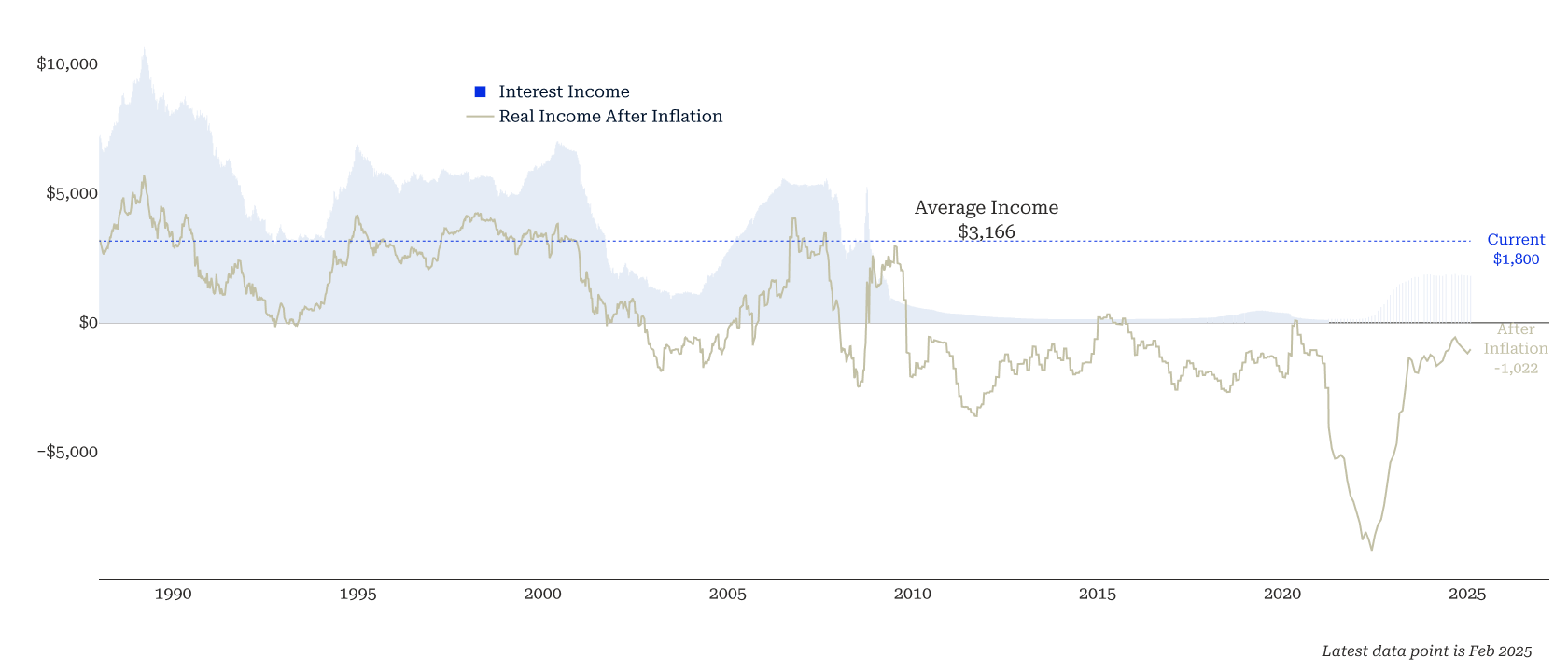

Moreover, traditional cash vehicles frequently provide insufficient returns once inflation is factored in (Figure 7). As historical data shows, interest income on cash often remains negative in real terms after accounting for inflation. While some cash instruments offer better yields, they are not a long-term solution for income generation or portfolio growth.

Figure 7: Interest Income on Cash

The Bottom Line

Trade policy shifts and market uncertainty can feel unsettling, but volatility is a natural part of investing. The Fed is maintaining a measured approach, balancing economic risks without overreacting. Likewise, long-term investors should stay the course.

The first quarter serves as a reminder of the value of a well-diversified portfolio – such as the Farther Dynamic Asset Allocation Models – in achieving financial goals. By maintaining a disciplined, long-term perspective, investors can navigate uncertainty with confidence and resilience.

Lauren Moone, CFA and David Darby, CFA contributed to this article.