After a sharp sell-off earlier in August (-6%), the S&P 500 rebounded (+2.3% for the month) and nearly returned to its all-time high in July. However, the index has declined over 3% month-to-date (as of September 9th) on economic data that continues to show signs of cooling.

With the Federal Reserve widely expected to begin cutting rates at their September 18th meeting, interest rates stabilized during the remainder of August after dipping significantly during the equity sell-off. Yields have declined month-to-date in September again, though, as investors resummed de-risking.

Given the uncertainty around the Fed’s full rate-cut path in the coming months, the upcoming presidential election, and ongoing geopolitical risks: here are 3 key takeaways to help investors navigate and prepare for potential volatility.

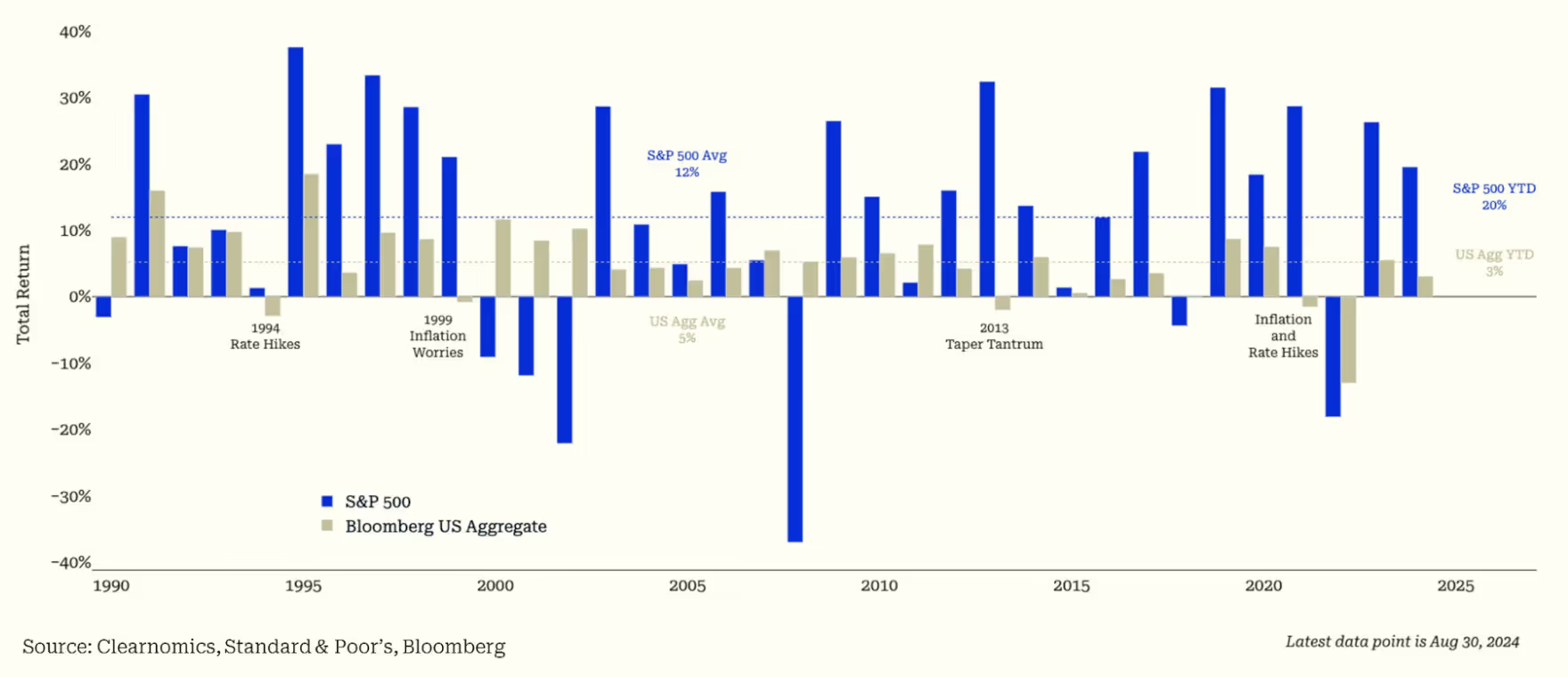

1. Both stocks and bonds have recovered in August.

Figure 1: Stocks (S&P 500) and Bonds (Bloomberg U.S. Aggregate): Total Returns

- Despite recent market swings, the S&P 500, Nasdaq, and Dow have gained 19.5%, 18.6%, and 11.7% YTD, respectively, including dividends (as of August 31st).

- The S&P 500 has experienced only two periods of sustained pullbacks this year, with the largest decline measuring 8%, well below the historical average of 13% annually.

- While mega-cap technology stocks experienced the sharpest declines during the early August sell-off, they also rebounded the most and outperformed value, mid- and small-cap stocks for the month.

- Investors have shifted their focus back to corporate earnings, a key driver of equity returns, which are influenced by the broader economy. Earnings projections remain strong – with an expected growth rate of 10% for 2024 and nearly 14% over the next twelve months.

In anticipation of Fed rate cuts, bond returns have also improved after struggling much of this year (all numbers are as of August 31st):

- The Bloomberg U.S. Aggregate Index has gained 3.1% YTD and 6.7% since April, when the 10-year Treasury yield peaked around 4.7%.

- High-yield bonds are up 6.3% YTD, while investment-grade corporate bonds returned 3.5% and Treasuries 2.6%.

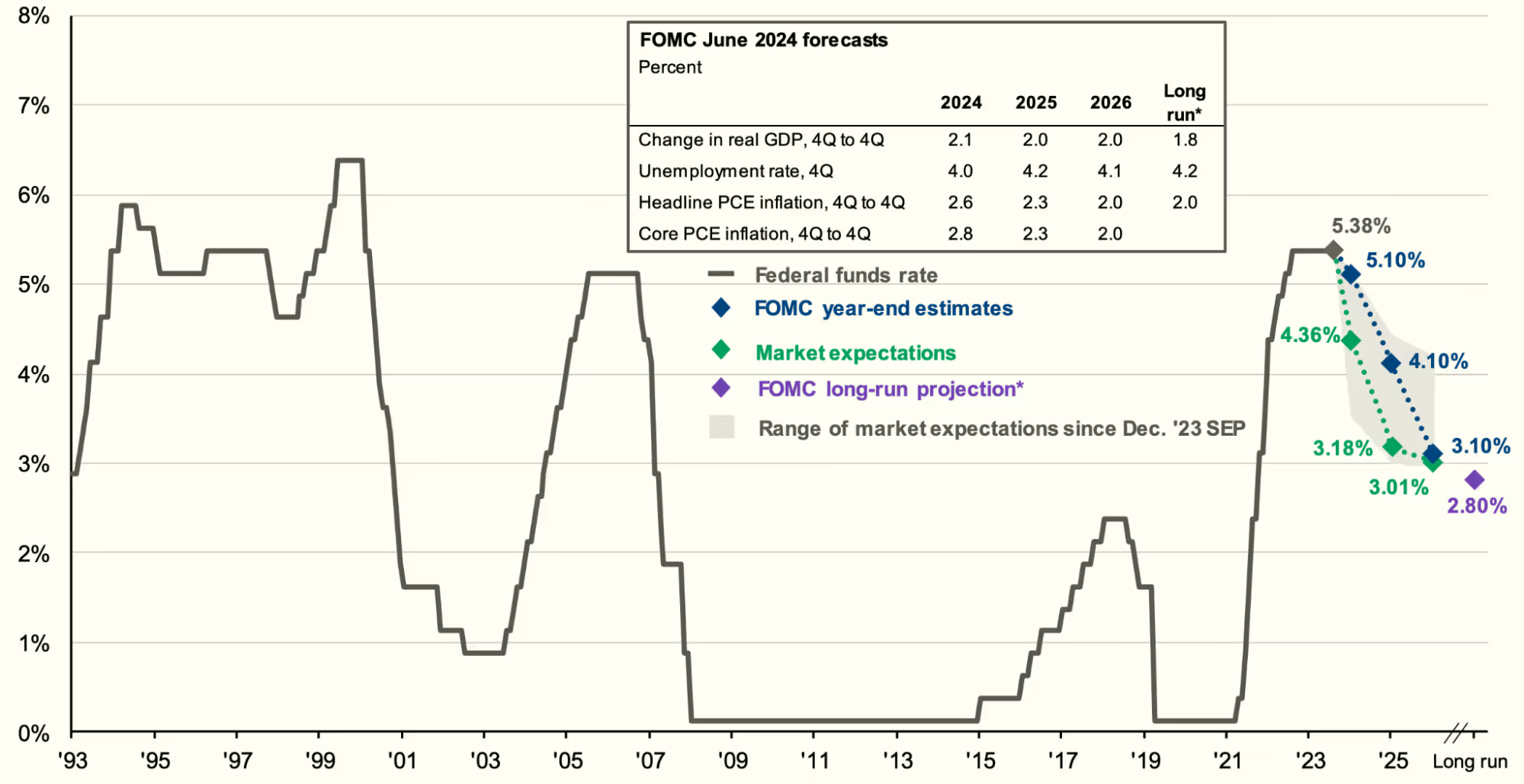

2. The Fed is expected to cut rates in September.

Changing expectations around the pace and path of Fed rate cuts have contributed to market volatility this year. Figure 2 illustrates the wide range of market expectations for interest rates since December 2023.

- At the beginning of 2024, investors forecasted several rate cuts due to concerns of a potential “hard landing.” However, when inflation ran hotter than anticipated in the first quarter, expectations shifted, and investors believed there would be no rate cuts this year.

- Now, the Fed is expected to cut rates by about 1% or more through the end of the year.

As these changing expectations have driven market shifts, it is crucial for investors to focus on underlying trends rather than reacting to macroeconomic changes.

Figure 2: Federal Funds Rate History and Expectations

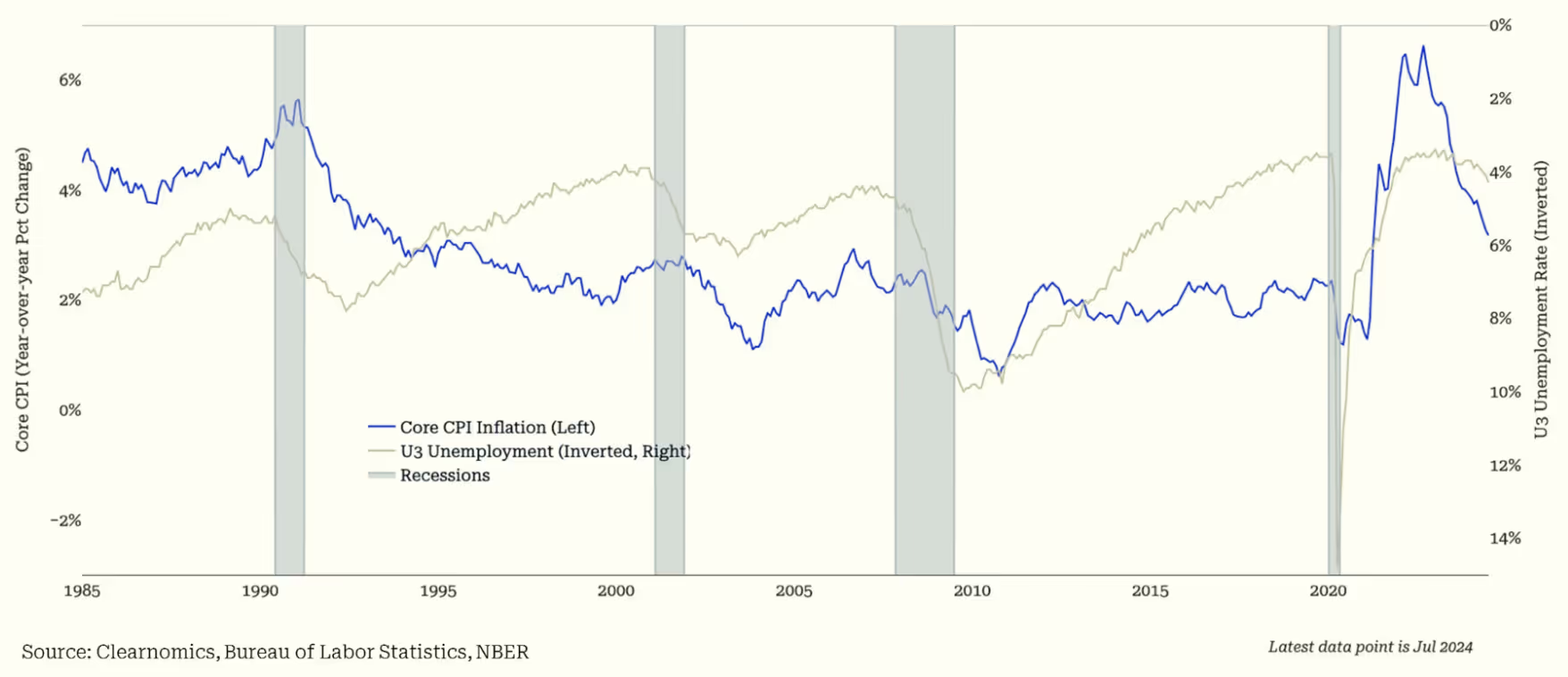

As inflation continues to decline, the Fed signaled that it will begin cutting rates later this month after a rapid rate hike cycle from early 2022 to mid-2023.

- The Fed’s preferred inflation measure, the Personal Consumption Expenditures Price Index, has decelerated to 2.5% overall and 2.6% when excluding food and energy, matching June’s gain and exceeding the 2.6% expectation.

- Similarly, the headline Consumer Price Index (CPI) fell to only 2.9% year-over-year in July, with the core CPI declining to 3.2%.

While consumer prices still remain higher than pre-pandemic levels, these improvements are sufficient enough for the Fed to justify a shift in monetary policy. Fed Chairman Jerome Powell recently stated: "The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks."

Previously concerned with bringing down high inflation, the Fed is now shifting its focus to the job market, which continues to soften gradually.

- In a recent speech, Powell discussed the downside risks of the job market, noting: “We do not seek or welcome further cooling in labor market conditions.”

- The unemployment rate fell a tenth of a percent to 4.2%, driven by a reversal of the temporary layoffs that were present in the July jobs report.

- The U.S. economy added 142,000 jobs in August 2024, 28,000 more than in July. That said, job growth over the prior two months was revised down by 89,000 jobs.

- The August employment report reinforces the view that the U.S. labor market is slowing but not breaking. It also reduced the likelihood of the “hard landing” scenario after the July jobs report.

- Immediately after the print, markets slightly increased the odds of a 50-basis-point move.

Figure 3: Unemployment (U3 Unemployment Rate, Inverted) and Inflation (Core CPI)

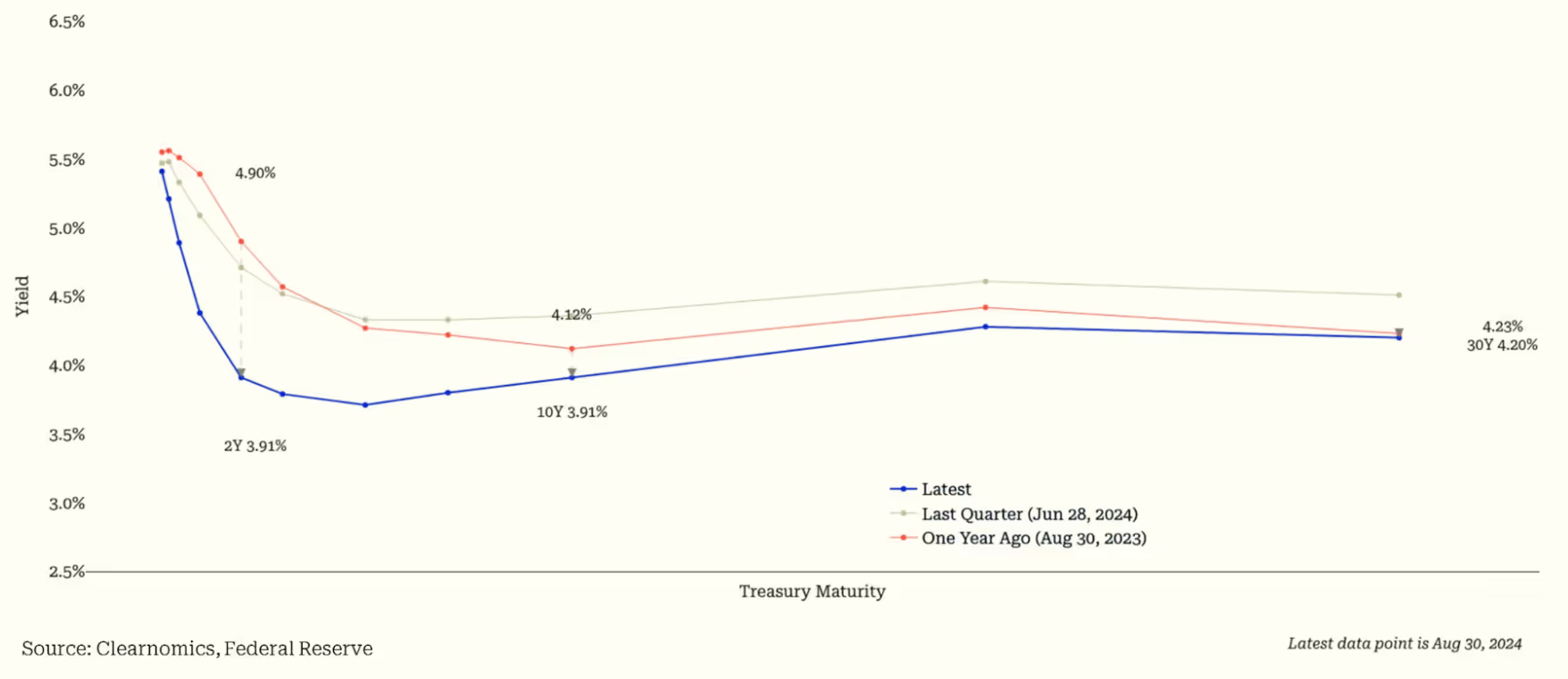

3. Interest rates are adjusting to a shift in Fed policy.

With Fed rate cuts approaching, market-based interest rates are also adjusting. Not only have yields decreased, particularly on the short-end of the curve, but the yield curve is no longer inverted. The spread between the 10-year and 2-year Treasury yields has turned slightly positive in early September.

If these moves continue, there could be potential implications for the economy and markets, including persistent recession fears. This year, some investors expected a recession, because the yield curve experienced its sharpest inversion since the 1980s. (Yield curve inversions have historically preceded recessions, since they typically occur later in the business cycle when the Fed has overtightened.) Although a recession is always possible, this instance might be different, since higher short-term yields were the result of inflation shocks.

While uncertainty remains, lower rates could spur economic growth – particularly in rate-sensitive areas such as real estate, technology, and small-cap equities. As discussed earlier, bonds have also benefited from improving rates, once again serving as portfolio diversifiers for investors.

Figure 4: The Shape of the U.S. Treasury Yield Curve

Farther Dynamic Multi-Asset Portfolios

At Farther, our advisors are maintaining diversified asset allocations that focus on long-term risk-adjusted returns, while also continuing to add positions to mitigate potential volatility. We encourage clients to remain fully invested with well-diversified portfolios, as missing the market’s upward movements could prove costly.

Lauren Moone, CFA and David Darby, CFA contributed to this piece.